When traffic is no longer a measure of success: metrics in the age of generative AI

AI-powered search systems are fundamentally changing online marketing: users receive answers directly in AI tools, and website traffic is declining. Companies must therefore use new KPIs such as brand mentions, citations, or entity coverage to accurately measure digital visibility and impact in the future.

The UX role: How AI is changing where UX creates value

AI-powered search systems are fundamentally changing online marketing: users receive answers directly in AI tools, and website traffic is declining. Companies must therefore use new KPIs such as brand mentions, citations, or entity coverage to accurately measure digital visibility and impact in the future.

Switzerland.com: Content as a service, not just information

Together with Switzerland Tourism, we revised the most important pages on Switzerland.com. The goal: to better support travellers when planning their trip or excursion in Switzerland. To achieve this, we focus on practical information and clear structures.

Understanding the buying centre in manufacturing: Why digital solutions fail without an understanding of roles

In manufacturing, buying centres decide on investments – with varying expectations of digital touchpoints. Anyone who designs customer portals or e-commerce for just one role will fail. This article shows why role-specific information, navigation and services are crucial for successful digital solutions.

Alumnus Markus – Criticism is welcome, but please make it constructive!

In our alumni series, alumnus Markus Haschka, Partner at Unic, explains why he is back at Unic. He talks about appreciation, corporate culture and how he would like to improve, change or advance Unic in his roles.

GraphQL, Kubernetes, jOOQ – How Gerald Wilhelm Works at Unic

The trickier the problems in software development, the better. Gerald Wilhelm, our code digger, has been working at Unic as an Expert Application Architect for over 17 years. In this spotlight, he talks about current technical trends, his activities on customer projects, and about the Unic team.

Typical CX challenges in manufacturing: Why technology alone is not enough

Many negative customer experiences in manufacturing are not caused by a lack of technology, but by fragmented system landscapes, organisational silos and a lack of end-to-end visibility of the customer journey. We show where the structural causes lie and how companies can address them in a targeted manner.

Customer Experience first: Digital transformation at Betty Bossi

How can SMEs successfully navigate digital transformation? Simon Balz, Head of Technology at Betty Bossi, explains why customer experience is the top priority in every project, what tomatoes have to do with digital transformation, and how roles change when AI suddenly takes over tasks.

Betty Bossi has been writing Swiss culinary history for decades. We had the privilege of contributing to the latest chapter: the digital transformation. In this dossier, we showcase what emerges when two parties bring their expertise to the table.

Why customer experience in manufacturing needs to be rethought

Manufacturing companies are digitising – but customer experiences often remain fragmented. The shift from product provider to solution partner requires new touchpoints, integrated customer portals and a rethink in sales. Why customer experience is becoming a strategic lever in manufacturing.

Martin Kriegler assists cooperative students in Karlsruhe as a coach

The education of specialised staff is an important matter for us. Therefore we are engaged as a cooperative partner of the Baden-Wuerttemberg Cooperative State University (Duale Hochschule Baden Württemberg - DHBW) in the major “IT".

9 Years of Holacracy – Martin Kriegler Takes Stock

What does the switch from the hierarchical corporate structure to the autonomous Holacracy organization, in which, as we know, there is no traditional management, actually entail? We asked Martin Kriegler, Expert Application Architect at Unic, what has changed in detail? And where Unic can still be optimized?

What exactly changes when a company transforms into the Holacracy organisational structure? How does the work of employees change? Patricia Gomez, Senior Application Architect at Unic, talks about the details and the challenges for the company itself.

Spotlight on – New Worlds of Work Require Mutual Trust

Sandro Dönni, Principal Transformation Consultant, talks about work-life balance at Unic, smart work and flexible working time models in a self-portrait.

What a Best of Swiss Apps Award Night: together with the TX Group and Graubünden Ferien, we looked back on the key moments of our projects, celebrated our collaboration and toasted two gold awards. The 20 Minuten app won gold and the Nordic Challenge "Alle laufen lang" also took gold. We congratulate the teams behind these extraordinary projects.

20 Minuten focuses on technical excellence: app relaunch successfully implemented

The collaboration between Unic and 20 Minuten on the relaunch of Switzerland's most-used news app is paying off: the app has been nominated for the Best of Swiss Apps 2025. The comprehensive redesign demonstrates the highest standards in mobile development and performance optimisation.

Unic expands strategically with the acquisition of Ludwigsburg-based digital agency Becklyn – 30 employees and three managing directors become part of Unic – New location strengthens German market position

Unic becomes a member of the "Souveräne Digitale Schweiz" (SDS) network

Zurich, 05.09.2025 - Unic, the specialist for digital platforms and applications, is now a member of the "Sovereign Digital Switzerland" (SDS) network. With this step, the agency is emphasising its commitment to digital self-determination and to independent and future-proof technology solutions.

The CX diamond: how to achieve strategic customer centricity without silos

Customer journeys are no longer just a buzzword - they are the key to sustainable customer centricity. However, many companies fail to create an overall strategic direction from individual journey fragments. At Unic, we have therefore developed the CX diamond as a methodological framework that combines four key dimensions.

While conventional tracking often only captures 35-40% of user data, Server Side Tracking (SST) enables significantly higher data quality and quantity. The capture rate also varies greatly depending on the industry: from 30-40% in retail to significantly lower values in regulated industries such as finance. In our practical test on Unic.com, we compared various SST solutions and gained concrete insights for practical application.

I couldn't believe it. A single sentence - and the system was supposed to handle a complete train booking? When I tested the new agent mode of GPT-5 with the Jungfrau Railway website out of professional curiosity, I was skeptical.

Search Everywhere Optimisation: Lead your SEO strategy into the future

The digital search landscape is changing fundamentally. Search Everywhere Optimisation extends the classic SEO strategy to make your brand visible on all relevant platforms - from traditional search engines to LLMs such as ChatGPT and social networks.

The Apple Worldwide Developers Conference (WWDC) 2025 kicked off with a keynote speech at the beginning of June, and of course, as app professionals, we listened closely. Here we share the most exciting innovations that could excite Apple users and app developers.

Internet Agency Ranking 2025: Unic continues successful ascent

Unic Germany improves from 41st to 40th place in the BVDW Internet Agency Ranking 2025 and climbs to 11th in the e-commerce ranking. Despite challenging market conditions with declining industry revenues, the agency solidifies its position in the top 30% of all participants. Continuous rise from 105th place in 2014 to 40th today. Success through strong technology partnerships and expertise in CX and UX topics.

Unic supports you in the introduction and further development of your individual AI solution - including the desired added value, which we realise in a short time.

How the Post Makes Over 750,000 Messages Per Day More Understandable

Swiss Post has redesigned its daily 750,000 shipment notifications. With a clear structure and user-centric approach, messages became more understandable and action-oriented. Status updates evolved into genuine service, customer satisfaction rose to 4.5 out of 5 stars, and support inquiries decreased. The project demonstrates: Well-thought-out communication creates added value for both the postal service and recipients.

On-Demand-Webinar: CMS, DXP & Co: Choosing the right foundation

Are you wondering whether your current CMS is still up to the increasing demands? And what advantages modern solutions offer? Or would you like to learn how a CMS selection is carried out systematically and strategically – and which aspects really count?

The era of the platform economy: learning effects for B2B companies

Digitalization has established a new economic model: the platform economy. What was originally perfected by B2C companies such as Amazon, Uber or AirBnB now offers valuable impetus for manufacturing companies with a B2B focus. Which key attributes of successful platforms can B2B companies use for their own digital transformation? And how can these be implemented in practice?

Mobile Apps in Industry: Revolutionizing Customer Experiences and Internal Processes

Mobile apps are revolutionizing the industry by enhancing customer experiences and optimizing internal processes. With apps, companies can offer seamless shopping experiences, maintenance support, and immersive technologies to customers, while also boosting efficiency in quality assurance, logistics, and communication.

Digitalisation trends in the manufacturing industry: rethinking the customer experience

The manufacturing industry is in the midst of a digital transformation that is not only changing internal processes, but also the way in which companies interact with their customers. At the centre of this development is the customer experience (CX) - in other words, the interaction of all digital and physical touchpoints along the customer journey.

Why, How, What - Business and sustainability in harmony

Do you know Simon Sinek's Golden Circle? In 2006, Sinek put forward the thesis that successful companies begin their business ideas or product visions with the “why”. According to Sinek, the why is the central belief and the most compelling reason why we do something. The model consists of three central questions: Why, How and What. At Unic, we have not only adopted the “Why, How, What” model, it is the basis of our Unic identity.

AI agents are coming: How to get your website ready

Imagine this: A potential customer commissions a digital assistant to analyse your products and compare them with those of the competition. This is not science fiction - it will soon be part of everyday life, thanks to AI agents like OpenAI's Operator.

With the introduction of such AI agents, it is becoming increasingly important to optimise your website not only for humans, but also for digital assistants.

E-E-A-T optimisation: SEO guide for more visibility on Google

While the internet continues to be flooded with AI-generated content in 2025, the value of authentic content rises. Google's E-E-A-T criteria help you demonstrate quality and expertise. We explain how to improve your visibility in search results.

How ChatGPT will change web search and user behaviour

ChatGPT, Perplexity and Claude are establishing themselves as alternatives for daily searches on the web. As a result, traditional search engines are facing competition and this is having an impact on companies' marketing strategies. Here we explain why we believe search engine optimisation (SEO) is becoming even more important and what optimisation for language models and AI tools could look like for your company one day.

The SBB Mobile app is one of the most successful digital applications in Switzerland, boasting an impressive 3.5 million active users monthly and 300,000 tickets sold daily. As the highest-grossing sales channel of Swiss Federal Railways, it is at the center of public interest.

Zurich Airport – Recognition as the best airport website worldwide

Zurich Airport’s website has been named “World’s Best Airport Website” at the 2024 World Travel Tech Awards. Recognized as one of Europe’s best since 2022, it excelled globally this year with its user-friendly design, innovative tools, and up-to-date flight information.

Does Your Website Fulfil the New Legal Requirements for Accessibility?

From mid-2025, websites that provide electronic services must be accessible. This is stipulated in the German Accessibility Reinforcement Act (BFSG), implementing European guidelines. The law also affects Swiss companies that offer products and services in the EU or Germany.

In this blog post, we explain who is affected by the changes, what you need to look out for to be compliant and how you can evaluate your website with our handy checklist.

How does Holacracy affect companies? What experiences do employees have with this hierarchy-free organisational structure? It has now been seven years since Unic transformed into this form of organisation. Time to take stock. Sandro Dönni, Principal Consultant at Unic, answers our questions and talks about his experiences with Holacracy.

What does the switch from the hierarchical corporate structure to the autonomous Holacracy organisation, in which, as we know, there is no traditional management, actually mean? We asked Melanie Klühe, Client Partner at Unic, what has changed in detail? And where Unic can still be optimised?

DRUPA 2024 review: Three trends in print manufacturing

DRUPA, the world's leading trade fair for printing and finishing machinery, attracts experts to Düsseldorf every four years to Düsseldorf every four years. This year's event showcased three key trends that are shaping the future of the industry: Workflow automation, real-time analyses and digital customer portals. We go into the details in the following blog post.

What does the switch from the hierarchical corporate structure to the autonomous Holacracy organization, in which, as we know, there is no traditional management, actually entail? We asked Dirk Nölke, Principal Consultant at Unic, what has changed in detail? And where Unic can still be optimized?

Sitecore OrderCloud – Insights Into a Highly Flexible E-commerce Platform

Die Sitecore OrderCloud überzeugt Kund:innen mit schnellen Entwicklungszyklen, ihrer Flexibilität und ist mit ihrer MACH-Architektur absolut zukunftsfähig. Wir stellen im folgenden Beitrag das Enterprise-Shop-System vor und gehen dabei auf die einzelnen Vorteile bzw. Features ein.

What makes alumni return to the company? What is their motivation to come back? We asked Melanie Klühe about her reasons for returning. The senior sales consultant shares interesting insights in this interview.

In March 2024, Unic opened the Spatial Lab in Zurich, a space to test Apple Vision Pro and learn about the ‘Spatial Discovery Canvas’: This workshop helps companies develop concrete ideas and test their feasibility.

From Wholesale to Retail: B2B Companies Conquering D2C Territory

Companies that previously relied exclusively on a partner sales model are increasingly being forced to rethink their strategy. In particular, direct sales to end customers, or D2C for short, is proving to be a lucrative sales channel. In the following, we explain the opportunities and challenges associated with a business model based on D2C.

Unic as a sparring partner for New Work at the Institute of Physiotherapy, ZHAW

The Institute of Physiotherapy has been part of the Department of Health at ZHAW Zurich University of Applied Sciences since 2006. Teaching and research prepare students and continuing education participants under one roof for the challenges in healthcare: practical-clinical or research-oriented. The organizational structure is new: Since February 2021, Unic has been supporting the Institute in transitioning to a role-based organization, inspired by holacratic principles.

Digital Platforms: Design, Concept, Implementation

Your website and digital services are key elements of your company’s profile and long-term success. To meet all these requirements, you need a solution based on modular architecture: High performance today and strong potential for the future.

Spotlight on – Home office with digital team spirit

Marc Steinhoff talks about how he balances his job and family within Unic - and why the team and teamwork itself are so important to him, whether in the home office in Hamburg or, if necessary, in the office in Zurich.

Spryker Hackathon – Chatbot Component for the Commerce System

The Spryker Excite 2023 in Berlin was coming up and of course a small team of Unic was there. Besides good conversations and great presentations, two developers and their team set out to develop a chatbot component including AI functions during a hackathon - with success.

Connect 2023 - Takeouts – Product Data is Fundamental to the Customer Experience in E-commerce

At this year's Connect, we had the pleasure of presenting the successful SWISS-KRONO project, which we realized with a PIM system from Akeneo, together with the SWISS Krono Group. Below you can read my takeouts from the presentation.

Internet Agency Ranking 2023: Unic Improves Position and Revenue Through Sustainable Growth

The internet agency ranking by the German Association for the Digital Economy (Bundesverband Digitale Wirtschaft – BVDW) is the industry barometer in the German internet agency landscape. Since 2001, the internet agency ranking has been compiled annually with partners HighText iBusiness, Horizont and werben & verkaufen. Unic Deutschland improved its position in the latest ranking and is now ranked at 53 with a revenue of EUR 10.8 million.

Thanks to a mobile workplace with no "hard" attendance requirements, Patricia finds it much easier to cope with everyday challenges. In the self-portrait, she also reveals what else Unic has to offer in terms of work-life balance.

AI – Hype or Opportunity for a Digital Agency? A Look Behind the Scenes.

There has been a lot of talk recently about artificial intelligence and possible applications of generative AI. The race is on. Is it just hype – or a real opportunity for a digital agency such as Unic? We talked to Ivo Bättig, innovation enabler, transformation consultant and partner at Unic, to learn more.

The Excellence in Business Impact Award is presented annually by Sitecore, a leading provider of modular content management systems and a partner of Unic. The award goes to digital agencies that provide outstanding services with Sitecore technologies. This year, Unic was the only Swiss agency among the winners.

Psychological Security and New Work – or How to Make Shared Governance Work

Experts and interested professionals got together at an after-work event in Berne to talk about psychological security and shared governance. What do employees and (former) managers need when responsibilities are shared in a novel way? Here are a few tips on how to make shared governance work.

Writing With the Support of Artificial Intelligence

Whether it’s blog posts, product descriptions or emails, artificial intelligence can already take over a lot of our writing. Nadia Meier shows some of the possibilities.

Can you trust your data? Our analytics audit will help you

We offer an analytics audit: We test your analytics tool and analyze the data quality in your company. This way you can be sure that your data is correct and forms the right basis for your online strategy. Contact us for an analytics audit.

Kubernetes is often referred to as an operating system for cloud applications. However, there is more to the ecosystem: we will go into more detail below.

Below, we take a closer look at the customer experience (CX) and explain why a positive CX is more important than ever. Another aspect is the effectiveness of customer experience management (CXM). The article includes practical examples and strategic insight to provide valuable input on how companies can create consistently positive customer experience to set themselves apart from the competition.

Cloud computing has become an important tool for companies to offer services and technologies to companies and customers regardless of the operating system. In other words, to offer their core business digitally via their own digital platform. We show what the digital cloud describes.

Measuring the Right Data: How Jean-Marc Bolfing Works

What is actually done at Unic? We created the column “A look over the shoulder” to provide an look behind the scenes - from the point of view of different roles at Unic.

What is Data, What is Information? Here’s The Difference?

Data are loose signs or symbols, while information has a meaning and represents a value for the recipient. We look in detail at the questions; what is data, what is information?

What is a frontend and what is a backend? How do we actually interact with a website? And how does data management work in the backend? We explain this in the following Wiki article.

What is User Experience (UX)? What is a User Interface (UI)?

User experience (UX) and user interface (UI) are terms that play a central role in web and app development. But what exactly do the abbreviations UX and UI mean? And how are they connected? We will go into detail below.

Omnichannel, also known as omni-channel, revolutionizes online retail by seamlessly connecting various digital and physical sales channels. All channels merge together, providing systematic linkage and accessibility to all relevant information. We will explore each channel in detail and highlight their advantages and disadvantages.

Targeted marketing in compliance with the current data protection regulations and the future Swiss data protection law. Is that possible? And if so, how? We discuss this in this article.

In the run-up to our e-commerce projects customers often ask, “How do you define an MVP at Unic?” We have outlined our take below, introducing the key success factors for a viable MVP in the context of digital sales.

In February 2022, after an extensive planning phase, our colleagues in Bern moved from the old Unic office on Eigerplatz to VIDMARplus in Liebefeld. A conversation with those responsible for the project.

A design system is more than just a framework with clear rules and reusable components. We will go into the definition in detail below. We look at its components and why a design system actually makes sense.

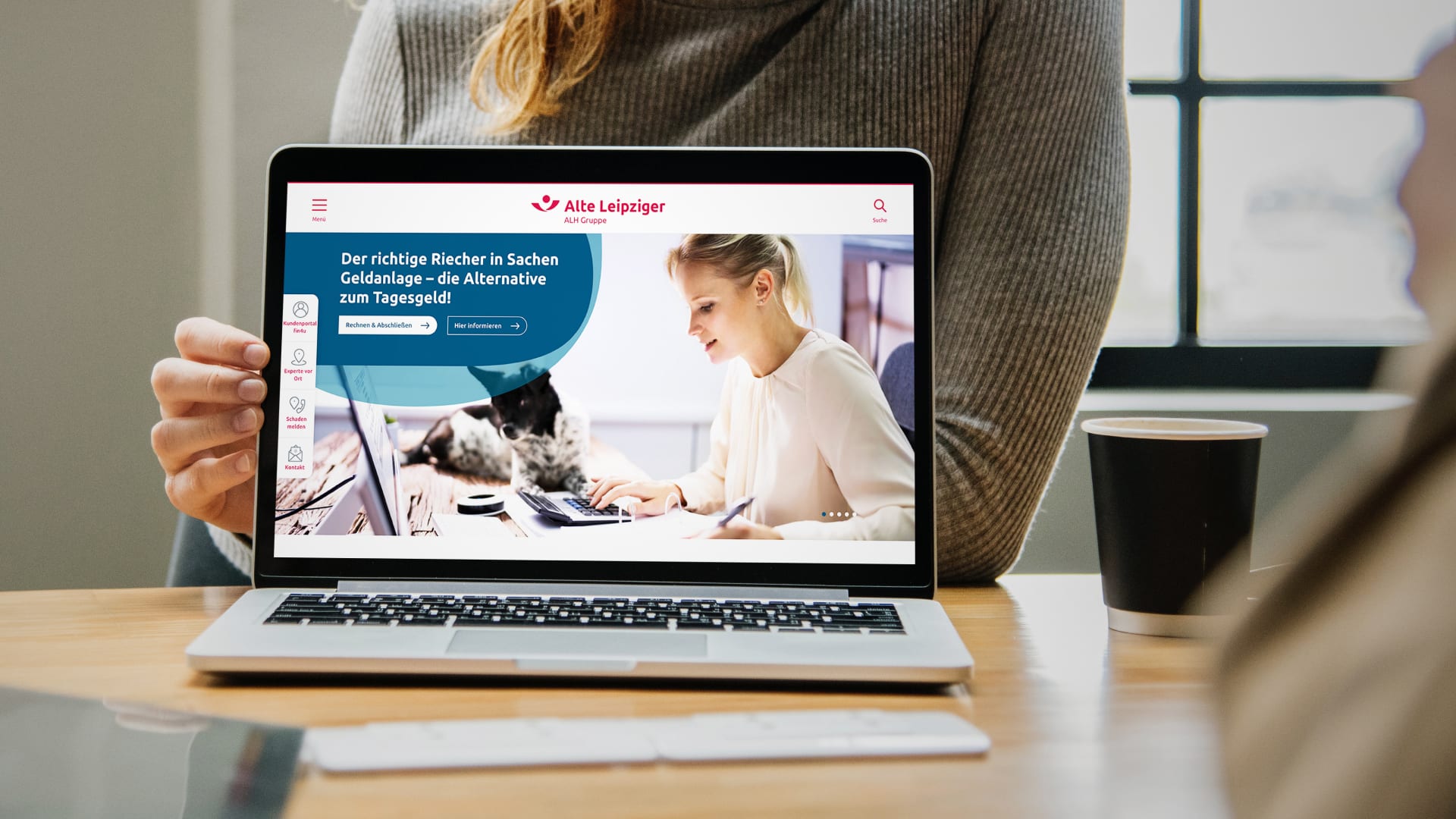

As part of a brand relaunch initiated in 2020, the Alte Leipziger-Hallesche insurance group hired us to redesign their existing website. Below is an example of a model approach to this request, using a content management system.

E-commerce refers to electronic commerce using Internet technologies, including the purchase and sale of goods and services in the business-to-business and business-to-consumer segments. We go into more detail in the following article.

Although Content is a crucial business asset there is often no comprehensive approach to the content lifecycle. Here are six common challenges in content management and how to master them.

Enhancing the Intelligence of Your Conversational Interface or Chatbot

Conversation is everything. For this, chatbots and conversational interfaces need to be designed, configured and trained. That's how chatbots are getting smarter – at least a little bit.

What is Headless? We will show you the different aspects and areas of the new technology. A Headless CMS decouples the frontend from the backend using an API.

Unic & Swiss Post – 20 Years of Shared Web History

For more than 20 years now, we have been supporting Swiss Post in all their digital endeavours. So far, we have implemented four relaunch projects and around 400 other projects for Swiss Post. And our journey continues.

We Belong to the Best Swiss Digital Agencies – for more than 20 years

According to Netzwoche's list of best agencies, we are now ranked second among the best Swiss digital agencies. And this over the last 5 as well as the last 10 years.

One presentation at this years Front Conference especially stood out to me. „The HTML Treasure Hunt“ by the charismatic and profanity-loving Bruce Lawson. Let's talk about it.

In 21 years of working together, we have implemented countless projects, discussed ideas and initiated thoughts for JURA Elektroapparate AG. A good time to look back on the years we have spent together.

Together with CSS we picked up this coveted award for the best Swiss web project for the 5th time. We want to celebrate this moment. That's why we're revisiting our 5 master projects and reflecting on what unites the project teams behind these successes.

Headless at EnergieSchweiz: Where Everything Interacts

A headless content management system alone is not yet a website. A Kubernetes cluster cannot deploy anything on its own. It is only when architecture, code, tools, processes and people are allowed to interact that the adjustments made to the content in the CMS trigger an update in the statically generated website.

How to Generate More Traffic With Pillar Pages – an Example

High-quality content is always welcome. But what are users looking for and what kind of pages can help them find it? We take a closer look at a project we conducted with a client to show how we were able to increase traffic.

The digitalisation of HORNBACH, initiated with Unic in 2009, wrote history, not just in terms of Unic locations. In this interview, Unic senior project manager David Spark tells us why this partnership has been such a success. He also explains how Unic’s customers participate in projects and turn their own ideas into reality.

For the relaunch of energieschweiz.ch, the editorial team invested a lot of energy into reworking the content. A content strategy, new formats and a content management system with headless architecture were a breath of fresh air for the web editing team.

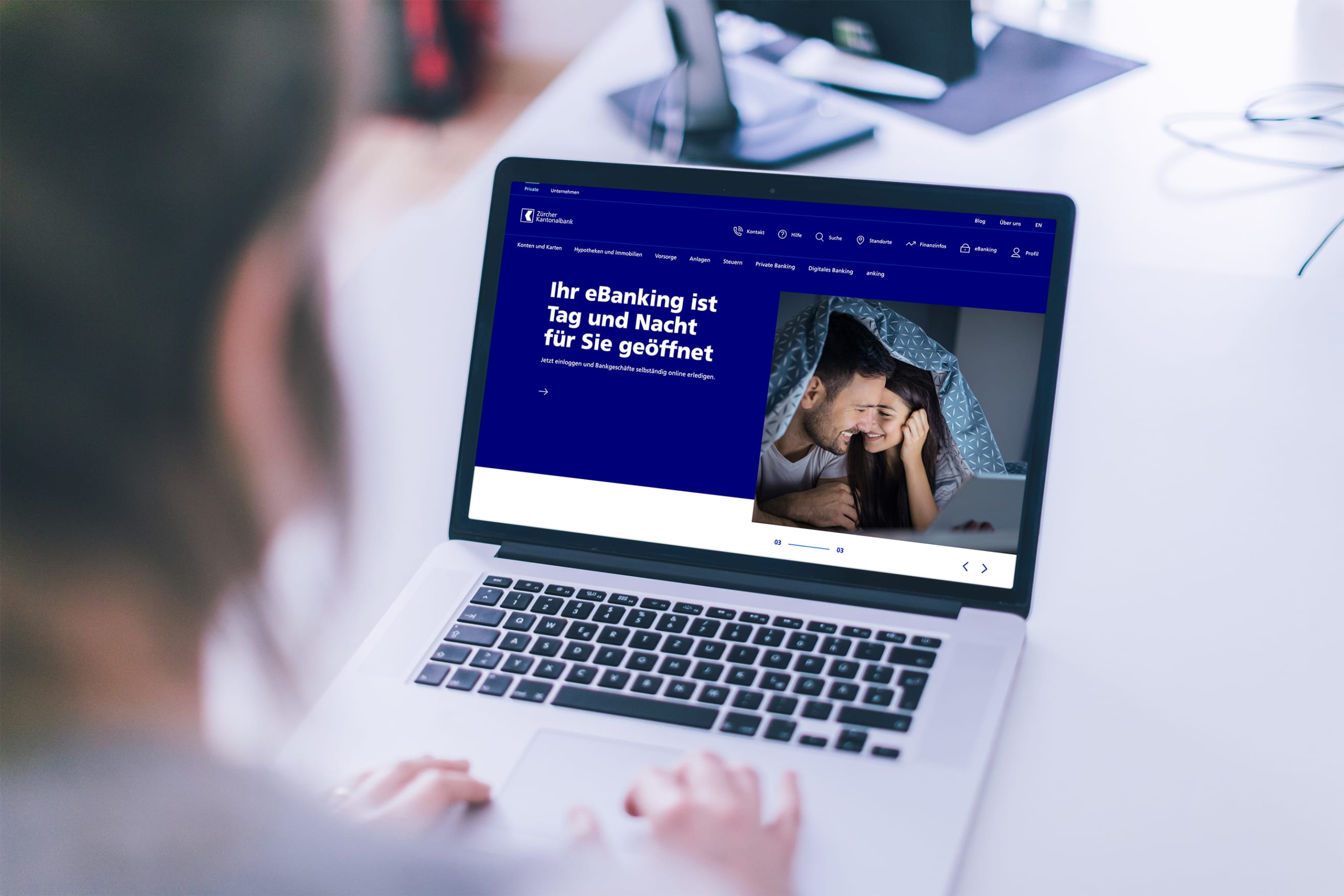

Content is at the heart of every digital platform. That is why Zürcher Kantonalbank (ZKB) placed a special focus on its content during the bank’s relaunch project. We supported Zürcher Kantonalbank in their content optimisation, including analysis, content generation and publishing.

Creating a Valuable User Experience from Data: How to Combine UX and Analytics

People often underestimate how valuable real data can be in the quest to improve the user experience of digital touchpoints. I have observed that many decision-makers do not harness the full potential of this data, even though user data is a direct source for the continual optimisation of a website or an online shop.

The new Zurich Airport website combines physical touchpoints with digital presence to create an integrated, personalised experience. What approaches and methods did we use to create a convincing user experience? Let me show you how a user-centric approach and an experimental mix of methods enabled us to do justice to both worlds.

Unic recently developed a completely new concept for UI design, user experience and frontend for Europa Möbel Verbund (EMV). In our interview, Elisabeth Starke (EMV), Florian Armbrust and Jutta Weber (both Unic) tell us about the approach that made the project successfully and explain why user experience is so important in product sales.

Content Management Combining Standard Features With Flexibility

50,000 content pages, 14 languages, 22 markets, 400,000 images and videos: These are impressive quantities for a content management platform. Peter Burkhalter, Senior Application Engineer, was in charge of technical design – an interview.

Establish a Product Vision to Make Your Digital Platform a Success

When you build or relaunch a digital platform, you have to meet countless different needs: it needs to support the journey of prospects and customers, contribute to business objectives and fulfil many other requirements.

In ten steps we explain how to create a content strategy, covering everything from analysis to the core strategy statement to content management. And you'll understand how important a content strategy is for your business.

Unic is celebrating 25 years in business – a quarter of a century that saw a lot of change, disruption and innovation. One thing that has remained a Unic hallmark all these years is the way we interact with others. We respect and appreciate others for who they are and value diversity.

"A new perspective is needed!" - UX experts in conversation

Stefan Pieren and Basil Bonzi are two Unic experts who examined the customer portals of the 12 leading Swiss health insurers as part of our new Service Design Report 2021. In the interview, they discuss why health insurance companies need to offer customer-centric digital services.

The collaboration on the Zurich Airport project brought an unprecedented level of communication. Marta Imos-Merska, senior software engineer in Poland, speaks about the international collaboration and technical challenges on the project from a back-end developer’s perspective.

Connecting Frontend and Backend with Contract Driven Development

While the concepts and ideas around headless CMS and its use cases are getting more wide spread, our Sitecore team started the journey on this topic by introducing Sitecore Javascript Services JSS for the multisite platform for Zurich Airport. Tobias Studer has explored the uncharted territory step by step and gives an insight into the considerations and challenges that shaped the final solution.

A Shiny Performance at the Best of Swiss Web Award Night

It was a special award night. Covid-19 dampened the party mood, but there were still many moments of jubilation for us. We are very happy about the brilliant balance: Our projects won 3x gold, 4x silver, 7x bronze and as a crowing touch the Master of Swiss Web.

We would like show how we have developed a state-of-the-art platform for Zurich Airport that opens many doors. We present the technologically innovative approaches of this interconnected multisite platform and try to shed light on the question of how decoupled Sitecore Headless really is.

Trivandrum – Wrocław – Bern: Three Countries – One Testing Team

Two time zones, three countries, three native languages, none of which is English. In the interview, our test manager Romy Maurer-Wysseier talks about the experiences of working together in an international testing team to prepare for the relaunch of the Zurich Airport platform.

How can you get the most out of your marketing budget over the long term? Here are 10 key metrics for measuring the effectiveness of your campaigns and finding out which advertising and communication campaigns are most successful.

Our Responsibility for Sustainable Digital Services

It is high time we take a closer look at the environmental footprint of digital services. This is not a new issue, but one that is becoming more relevant in the current situation as the COVID-19 pandemic has led to an explosion of data traffic volumes.

Setting New Digital Standards: Hoval's „Way to Cart“

Our customer, Hoval Aktiengesellschaft, is setting new standards with user-friendly ordering processes, thus supporting the shift from traditional to digital channels.

A functioning corporate design system requires real applications, real products and real customer feedback. Because we wanted to talk about service quality and product structure at Swiss Post, not about pixels.

Prepared for Disaster: Geo-redundant Hosting for Switzerland Tourism

Unic set up a second data centre for Switzerland Tourism to enable geo-redundant operation of MySwitzerland.com. Read the interview to find out what will happen to MySwitzerland.com in case of a disaster.

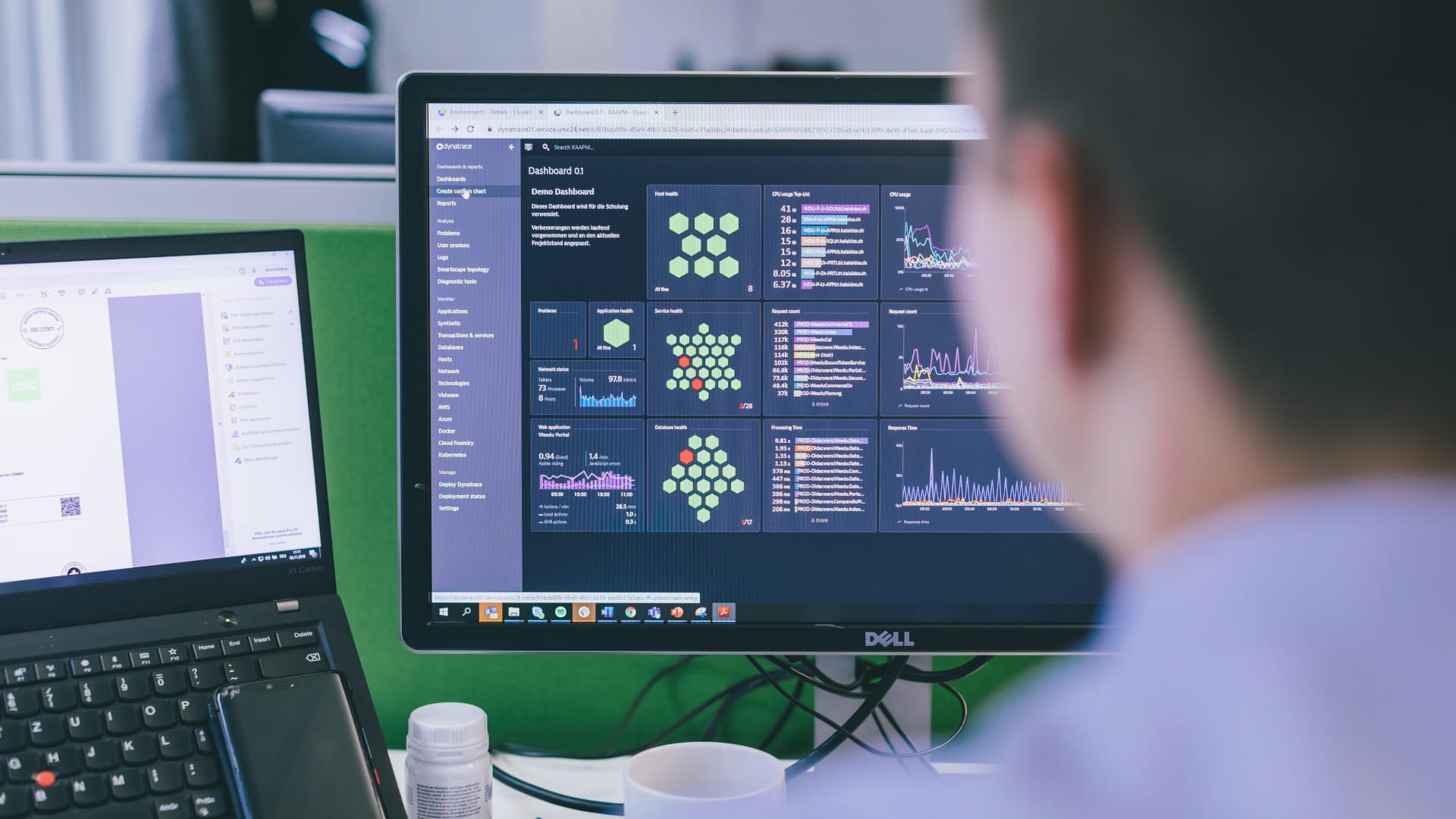

Dynatrace Named a Leader in Application Performance Monitoring

Dynatrace has once again been declared a leader in the Gartner Magic Quadrant 2020 for Application Performance Monitoring (APM). We are delighted to be able to help our customers achieve continued success with Dynatrace.

Our user research team wanted to quickly get an understanding of people’s new needs and behavioural patterns during the COVID crisis. To use the crisis as a window of opportunity to anticipate changes in the market. Read the results of this research here.

From Holacracy to Kanban to Objectives and Key Results – our journey into agile B2B marketing is not without some obstacles, but productive and goal-oriented.

How Does COVID-19 Affect User Behavior in the Online Supermarket?

The lockdown has had very different effects on the use of digital services in different sectors. We analyze the changes in online user behavior in the course of the lockdown in a small series. Part I: Online Supermarket.

How were the illustrations for the relaunch of post.ch created? Our UX designer Dorian Minnig, who was responsible for the illustrations, explains the rules.

“People Were Surprised That We Would Make Such a Big Change”

How to create a easy website that meets the needs of users and is even nominated for the Master of Swiss Web 2020? Roger Grüring and Silvan Bolli talk about the inner workings of a large-scale project.

Double Strike! Two of Our Sitecore Enthusiasts Are 2020 Sitecore MVP

We are proud that two of the „Most Valuable Professional Award“ are part of Unic: Tobias Studer receives the award as MVP Technology for the 5th time and Christian Hahnloser was awarded the MVP Ambassador.

Great joy right at the beginning of this year: SAP honors us, its long-standing partner Unic, as an SAP Gold Partner in addition to the „SAP Recognized Status“. We say „THANK YOU“ to SAP and explain what the Gold Partnership actually means.

Artificial Intelligence has become a standard in marketing. It is changing the way companies interact with customers but also requires marketers to rethink their self-image and skill set.

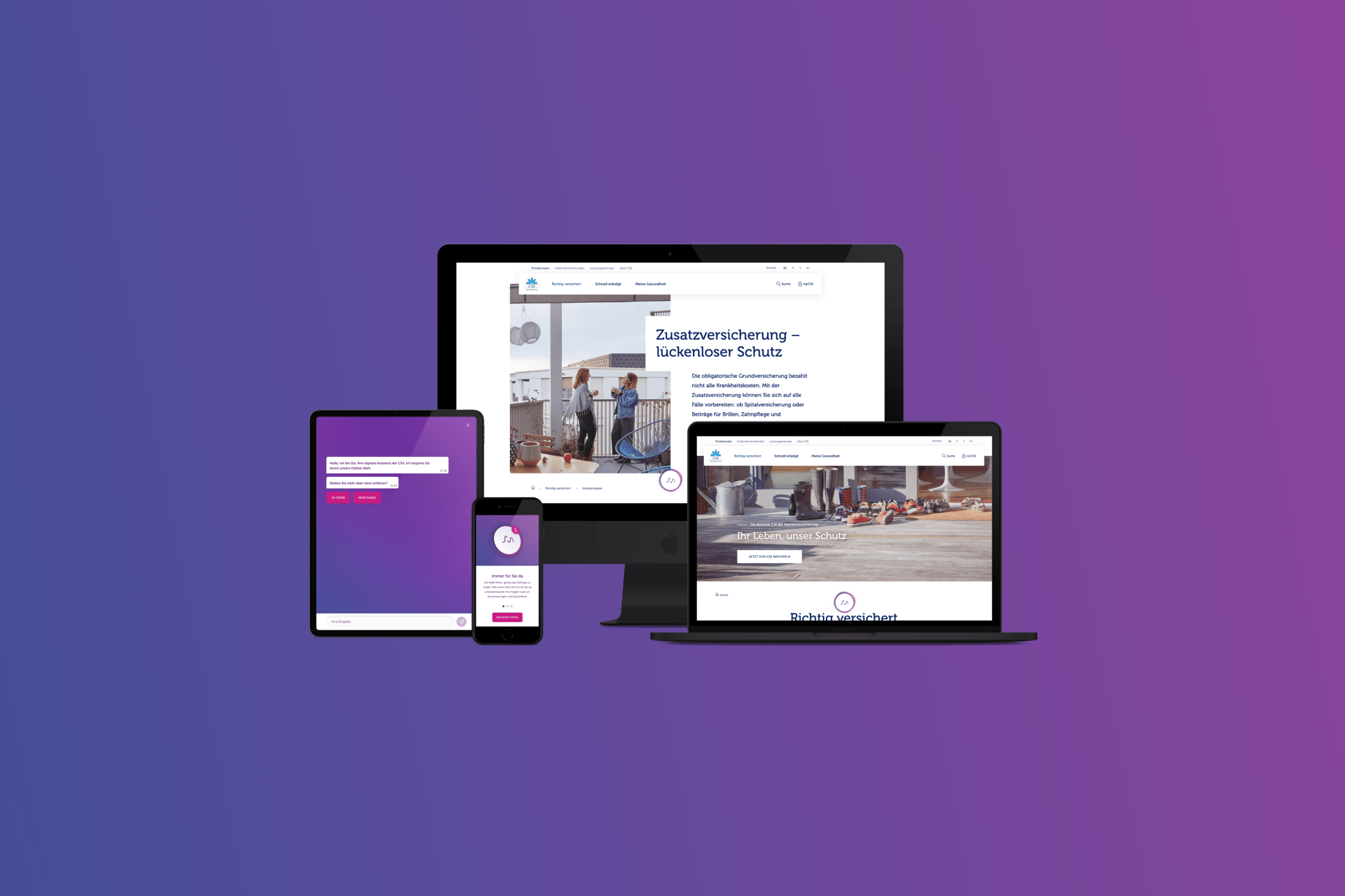

It is only by having smart user interfaces that valuable interactions can take place that "understand" customers on their journeys and support them in the best possible way. CSS Insurance wants to be one step ahead of its customers. To do so, it needs to know where its customers are and offer them useful options as they move forward.

Understanding the Users of css.ch: Research Methods and Findings

To design a responsive, relevant and user-centered web portal for CSS Insurance, it was essential to understand the users’ goals. Who visits css.ch? And what do visitors want to do on the website?

How smart are content management systems? And what do you need to do to reap the benefits from it? We looked behind the marketing facade and put Sitecore Cortex to the test.

Digital Ethics — the Conscience of Artificial Intelligence

When Dave the astronaut tries to reenter the spaceship in Stanley Kubrick’s “2001: A Space Odyssey” (1968), on-board computer HAL refuses to follow orders. “I’m sorry, Dave. I’m afraid I can’t do that.”

What does it take for Human-Centered Design (HCD) to work? That it does not just pay lip service? We have consistently carried out the optimization of post.ch in a user-centered manner. With prototypes and common principles.

The Elves of the Future: With Artificial Intelligence instead of Hats

In order to meet the increased demands on software and web applications, we use Application Performance Monitoring tools. These tools offer significant insight into the quality of solutions and support us in monitoring the systems – now with the help of artificial intelligence.

MySwitzerland.com: A Keen Eye for Innovation Serving Switzerland

Switzerland Tourism actively uses new technologies to provide its guests with continuous and needs-based support when they are planning their trips. Thomas Winkler and Markus Dittli from Switzerland Tourism spoke about their key ideas, innovation and the relaunch of MySwitzerland.com.

Artificial Intelligence: From Hype to Added Value for Customers

According to the latest Gartner Hype Cycle for digital marketing, expectations surrounding AI for marketing have reached their peak. The question at stake, however, is if AI really does offer added value that will stand the test of time once the hype has died down.

The ALTE LEIPZIGER – HALLESCHE Group Enters the Digital Age

The company has set a new standard in customer communication with the relaunch of its two websites. What better reason to take a closer look at the project in an interview!

As a cloud company, SAP continues to focus on establishing its experience products in its new cloud. But what is behind it, what are the advantages of the new cloud approach and what else is in store? We’ll explain in this blog post.

CSS aims to offer users a unique experience in the digital world: intelligent services that support users on their journey. To arrive at intelligent solutions, the approach to digital projects must be entirely different.

Why Artificial Intelligence is Not a Quantum Leap but Merely Makes Our Data-driven Work More Effective

Recording, interpreting and acting on data. Anything that artificial intelligence could one day do for us, we must first understand ourselves and be able to do on a small scale.

Artificial Intelligence of Things: How Intelligent Devices Change Our Lives

Thanks to the Artificial Intelligence of Things (AIoT), systems and devices have become data-driven, intelligent, automated and connected to the world. Is this just a gimmick or will it have a lasting impact on our lives?

This dossier shows how services become intelligent. It points out opinions on the potentials of artificial intelligence, but also how teams have to form in order to create intelligent services for customers. It examines various services with artificial intelligence and it analyses how much intelligence they really contain.

The formatting of images poses great challenges for content managers. AI can relieve this burden by automatically calculating the focal point. This ensures that the interesting image section always remains in view.

In the context of single-page applications and event-driven websites, there is often talk of Event Driven Data Layer (EDDL). Will EDDL replace the Customer Experience Digital Data Layer (CEDDL)?